The New Space Race Is Mostly a Subsidy Story

Space isn't a free market. It's industrial policy with better branding. Government funds development, covers failures, then celebrates private innovation.

Every few months, someone announces we're in a "new space race." Cue the dramatic music, the rocket porn, and the inevitable tweet about humanity becoming a multi-planet species.

Here's the less cinematic truth: a lot of the modern space boom is a subsidy story with better branding. It's procurement, contracts, tax incentives, and public risk—wrapped in a glossy "innovation" narrative.

The space industry loves telling you it's private and revolutionary. What it rarely mentions is that government remains the anchor customer, picking up the tab for R&D, assuming the risk, and then watching the upside get privatized.

What It Is

A space industry explainer on how government spending, regulation, and national strategy shape the "private" space industry—why "private" space is rarely private, and how the incentives determine what actually gets built.

Think of it this way: when politicians talk about the "free market" solving space exploration, they're usually describing a market where the government is the customer, pays for development, covers failures, and then celebrates private companies for "innovation."

This isn't a moral judgment. It's just where the money is. And where the money is, policy follows.

Why It Matters

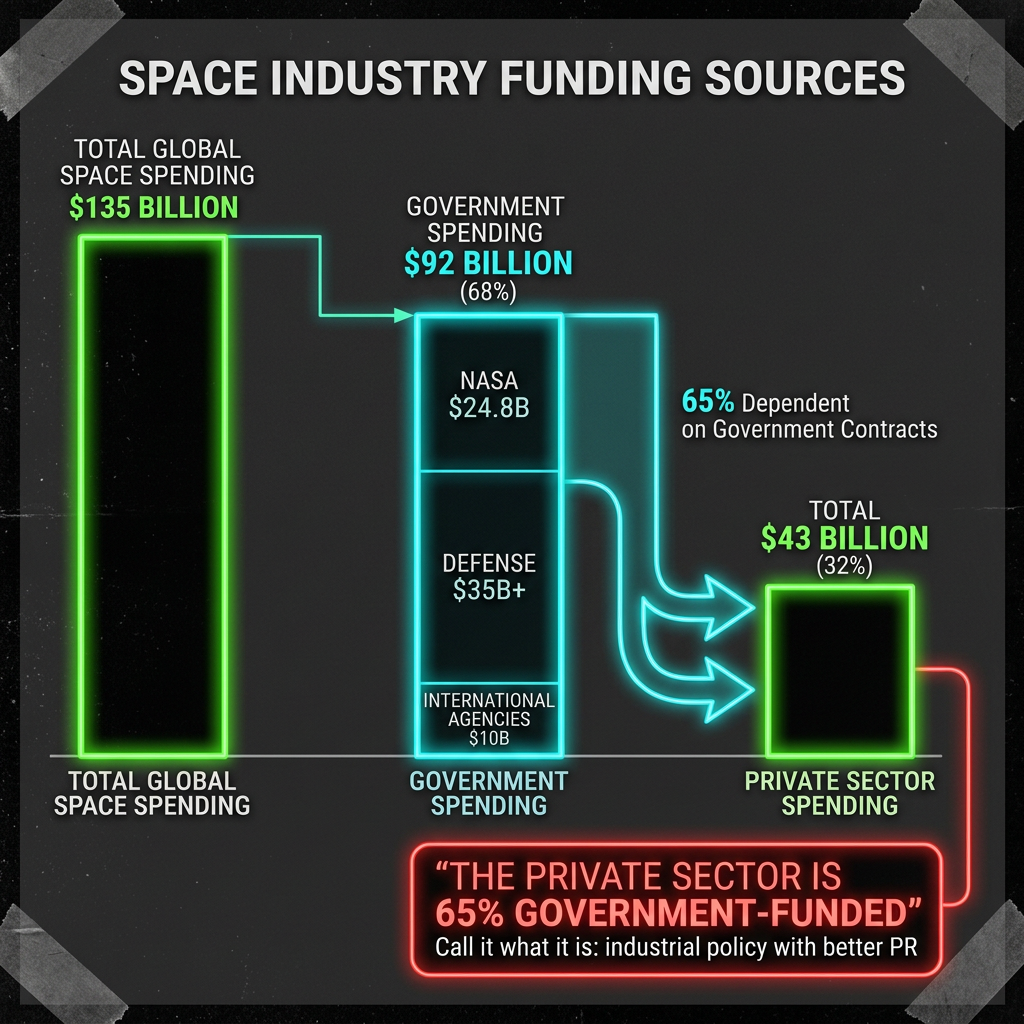

- Space budgets are public money; the benefits and risks should be public questions. NASA's 2025 budget is $24.8 billion. The Defense Department spends another $20+ billion on space. That's not pocket change. It's policy, made in public, with consequences. But the narrative around space is often treated as a business story, not a governance story. That's a mistake.

- National security and communications infrastructure are tied to space systems. Who controls orbit? Who decides what gets built up there? These are not free-market questions. They're geopolitical questions. And the companies involved operate under contracts, regulations, and national security classifications.

- The "space race" framing can obscure accountability: who pays, who profits, who decides. When something is framed as a race or a competition, it becomes easier to ignore the subsidies underneath. Easier to celebrate billionaires as visionaries. Harder to ask: who actually paid for this? Who benefited? Who took the risk?

Key Facts

Governments remain anchor customers for launches, satellites, and R&D.

NASA contracts with private companies for cargo resupply, crew transport, and lunar landers. The Defense Department buys launch services. Intelligence agencies buy satellite data. Without government contracts, most "private" space companies wouldn't exist. This is documented. It's not a conspiracy theory. It's procurement. Check the GAO reports if you want the receipts.

[Source: NASA FY 2025 Budget; GAO space acquisitions reporting]

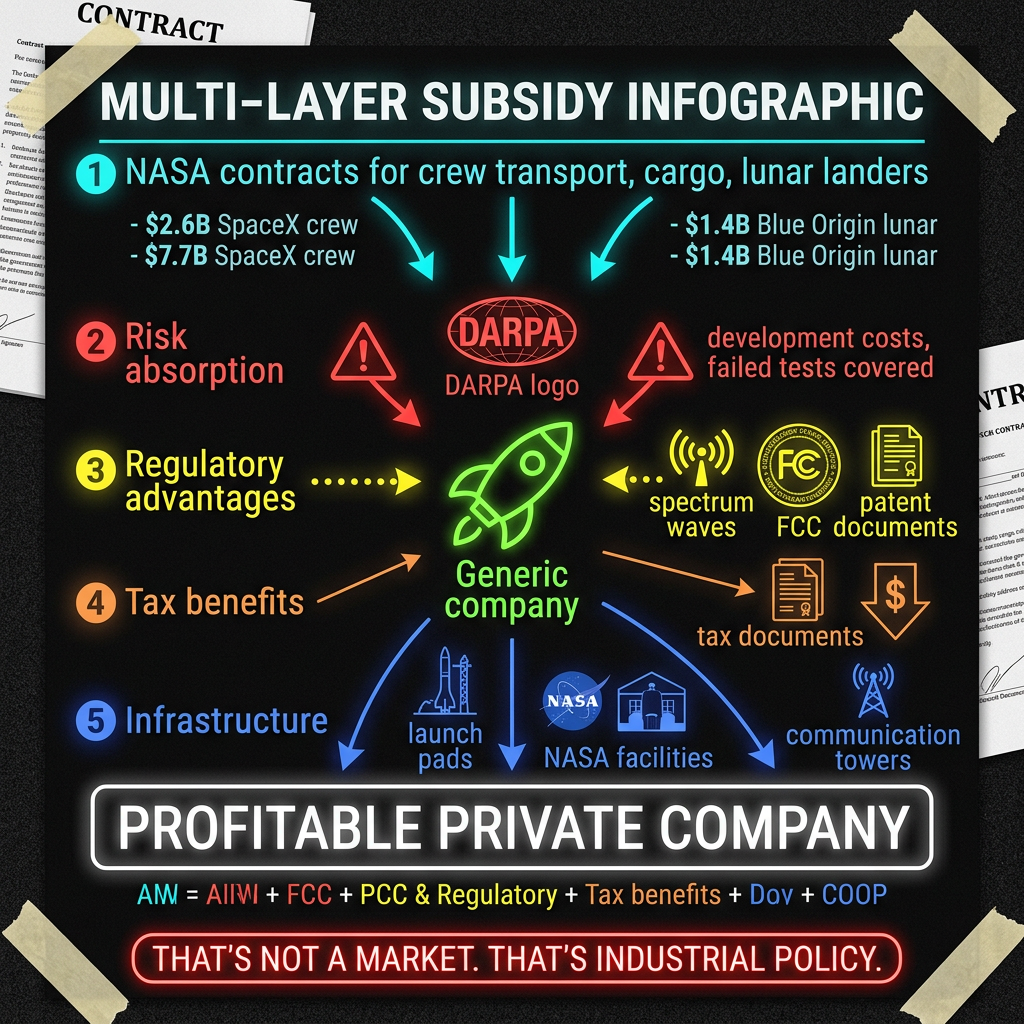

Many "private" breakthroughs depend on public research and risk absorption.

SpaceX's Raptor engines? Descended from decades of NASA research. Reusable rocket technology? DARPA and NASA funded the early work. Satellite communications? Military development led the way. Private companies are often good at manufacturing and optimization. But the fundamental R&D? That's typically public money, public risk.

[Source: Aerospace Corporation partnership analysis; space history documentation]

Government contracts shape industry direction: what gets prioritized is what gets funded.

When NASA decides to fund lunar landers, suddenly lunar lander companies proliferate. When the Defense Department prioritizes launch capacity, launch capacity becomes the competitive advantage. Companies optimize for what they get paid for. That's not cynicism. That's economics. The contracts are the strategy.

[Source: PNAS research on public-private partnerships in space]

Space is increasingly dual-use: commercial systems serve defense and intelligence needs.

A satellite constellation built for broadband? Also useful for surveillance. A launch vehicle optimized for commercial cargo? Also usable for military payloads. This is by design. The lines between "commercial" and "military" space are deliberately blurred. That's actually smart policy. But it's worth knowing that when you celebrate "private space innovation," you're often celebrating publicly-funded defense infrastructure.

[Source: Brookings Institution analysis on space policy]

The public absorbs risk; private companies capture upside.

When a development program fails, who eats the cost? The government. When it succeeds, who profits? The private company. This isn't unique to space. It's the structure of industrial policy everywhere. But space is a particularly clean example of the pattern: massive public investment, private capture of returns.

[Source: Financing the Space Economy reports]

Timeline: How We Got Here

Cold War era (1950s–1970s):

Space is state-led. NASA, NORAD, Soviet space program. Prestige + defense. The goal is to prove superiority. Cost is no object. Neither is failure. Both sides keep trying.

Post-Apollo deflation (1970s–1980s):

Space budgets shrink. NASA loses momentum. Interest fades. The "race" is over; the Cold War continues elsewhere. Space becomes routine.

Commercial experimentation (1980s–1990s):

Satellite communications start making money. Launch services begin to privatize. Reagan administration explores "commercial space." Private companies see opportunity. But the government remains the primary customer.

Reusable rocket dreaming (1990s–2000s):

X-Prize. SpaceShipOne. Private space advocates claim rockets can be made cheap. NASA and the military remain skeptical. Government contracts continue to be the main revenue stream. This period is full of hype and failure. Some companies fold. Others survive on government money.

Paradigm shift (2000s–2010s):

SpaceX succeeds with Falcon 9. Suddenly reusable rockets are real. Launch costs drop. The narrative shifts: "Private companies are disrupting space!" This is partly true. But what's not mentioned: SpaceX received extensive government funding, contracts, and technical support throughout its development. The "private" breakthrough was publicly subsidized.

Consolidation era (2010s–present):

Blue Origin, Relativity, Axiom, others emerge. Mega-constellations (Starlink, OneWeb, Kuiper) become feasible. Space tourism appears. The narrative: "Space is opening up to everyone!" The reality: most revenue still comes from government contracts, defense spending, and publicly-funded satellite programs. The market is real. But it's a government-created market.

So What: Three Patterns to Watch

Pattern 1: Follow the Customer, Not the Hype

If you want to know what's real in space, ask: who's paying?

- Launch contracts → Who has the money for launches? Governments. Private satellite operators launch on government-subsidized rockets.

- Broadband subsidies → Who funds mega-constellations? US government (Kuiper), international governments (OneWeb). Starlink is profitable partly because of government contracts and spectrum allocation.

- Defense procurement → The single largest driver of space spending is defense. Want to know what space tech gets prioritized? Follow military budgets.

The venture capital money is real. But it's the second wave of funding, not the first. Government risk comes first.

Pattern 2: The "Public Risk, Private Reward" Pattern

This is the core subsidy mechanism:

- Government funds R&D. NASA spends billions. DARPA develops technology. Military tests systems. All public money.

- Risk is assumed publicly. When development programs fail, taxpayers pay. When prototypes explode, we eat the cost.

- Success is privatized. When the technology works, private companies commercialize it, patent it, profit from it. Investors celebrate. Executives get rich.

This isn't unique to space. It's the American innovation model. But space is a textbook example: the entire reusable rocket revolution was publicly funded before it became "private innovation."

Pattern 3: Orbits, Spectrum, and Debris—The Next Fight

The "space race" narrative focuses on Mars and the Moon. The real fights are closer to home:

- Orbital congestion: Low Earth Orbit is getting crowded. Who gets to use which orbits? Governments and international treaties decide. That's policy, not markets.

- Spectrum allocation: Satellite companies need radio frequency spectrum. That's a scarce government resource. Governments auction it. Space becomes a regulatory game.

- Collision risk and debris: Every satellite launch adds debris. Every collision creates more debris. Eventually, orbit becomes unusable. Who decides cleanup? Who pays? These are governance questions, not startup questions.

The venture capital honeymoon in space won't last forever. When orbits start degrading, when debris becomes a real problem, when governments start enforcing regulations—that's when the "private space revolution" faces its actual constraint: the government can change the rules anytime.

What to Watch Next

- Regulatory tightening: Expect more government requirements around space debris, orbital traffic management, and licensing. As orbits get crowded, government control increases. "Private" becomes more constrained.

- International competition and consolidation: China and Europe are building alternative space ecosystems. That's geopolitical, not market-based. Consolidation in the US private sector will likely follow. Winners will be companies with government relationships, not necessarily the best technology.

- The broadband gamble: Mega-constellations (Starlink, Kuiper, OneWeb) are betting on satellite internet. Government money is fueling this (subsidies + procurement). If the market doesn't materialize as hoped, who takes the loss? That's the real test of "private" space economics.

- Dual-use everything: As space becomes more militarized and surveillance-intensive, the line between "commercial" and "military" space disappears entirely. Private companies become defense contractors. That's not innovation. That's consolidation.

The Practical Takeaway

When you see headlines about the "new space race" or "private space companies disrupting the industry," remember: most of the money is still government money. Most of the risk is still public risk. Most of the infrastructure is still public infrastructure.

This isn't a criticism of the space industry. It's a description of how American industrial policy actually works. We fund big, risky, long-term projects through government contracts, assume the risk publicly, and then celebrate when private companies commercialize the results.

In space, that model has actually worked pretty well. Reusable rockets are real. Launch costs have dropped. New companies have emerged.

But the narrative—that this is "free market innovation" competing against government inefficiency—is a story, not a fact. The real story is more interesting: government strategy + private execution + public money = space economy.

Understand the subsidy structure, and you understand what's actually going to happen next.

Sources

- NASA FY 2025 Budget Fact Sheet. https://www.nasa.gov/wp-content/uploads/2024/03/fy-2025-budget-agency-fact-sheet.pdf

- The Planetary Society. "NASA's FY 2025 Budget." https://www.planetary.org/space-policy/nasas-fy-2025-budget

- Washington Post. "Elon Musk's business empire is built on $38 billion in government funding." https://www.washingtonpost.com/technology/interactive/2025/elon-musk-business-government-contracts-funding/

- ProPublica. "SpaceX Took Money Directly From Chinese Investors." https://www.propublica.org/article/elon-musk-spacex-china-investors-court-testimony

- Norton Rose Fulbright. "Financing the Space Economy." https://www.nortonrosefulbright.com/-/media/files/financing-the-space-economy.pdf

- Government Accountability Office. "Space Acquisitions." https://www.gao.gov/products/gao-13-802r

- Aerospace Corporation. "Public-Private Partnerships: Stimulating Innovation." https://aerospace.org/sites/default/files/2018-06/Partnerships_Rev_5-4-18.pdf

- Brookings Institution. "Industrial Policy for the Final Frontier: Governing Growth in the Emerging Space Economy." https://www.brookings.edu/articles/industrial-policy-for-the-final-frontier-governing-growth-in-the-emerging-space-economy/

- Brookings Institution. "How Space Exploration Is Fueling the Fourth Industrial Revolution." https://www.brookings.edu/articles/how-space-exploration-is-fueling-the-fourth-industrial-revolution/

- PNAS. "Public–private partnerships in fostering outer space innovations." https://www.pnas.org/doi/10.1073/pnas.2222013120